Solid dividends

Dividends still carry risks

regain popularity

as growth stocks fadeBy Dave Segal

dsegal@starbulletin.com

"I have a philosophy that life is just not adding zeros to your bank account. Life is adding quality. Money is a means to an end where you take your hard-earned savings and investments so you get returns on them, and use the returns to take a cruise, enjoy meals or give to charity."

-- Paul Loo, senior vice president, brokerage Morgan Stanley, HonoluluDividends, snubbed in the 1990s as investors piled into growth stocks, are back in vogue again.

And that means shareholders are once again paying attention to the total return of their investments.

The bear market -- the catalyst for this reawakening -- has left many investors scrambling for guaranteed income after watching their portfolios shrink by 50 percent or more.

"When growth slows down or growth doesn't look as reliable as it did, people obviously turn to dividends," said Paul Loo, senior vice president of brokerage Morgan Stanley in Honolulu. "I like to get some dividends. And I like to get them in the mail so I can have the chance to spend them."

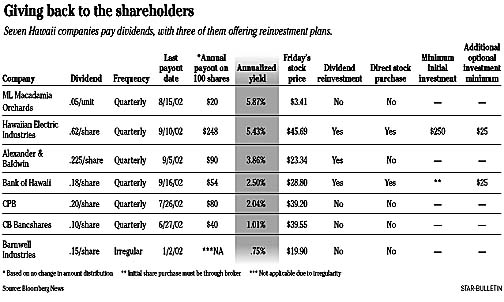

In Hawaii, seven of the state's 12 largest publicly traded companies offer dividends in yields ranging from just under 1 percent to nearly 6 percent. Additionally, three of the companies offer dividend reinvestment plans, more commonly known as DRIPs, which allow stockholders to have their dividends automatically reinvested in additional shares.

The state's largest dividend reinvestment and stock purchase plan, administered by Hawaiian Electric Industries Inc., has more than 28,000 participants and enables participants to bypass brokerage commissions and buy shares directly from the company. The stock purchase plan requires a minimum initial investment of $250 with additional optional cash investments of at least $25 per transaction.

Bank of Hawaii Corp., with approximately 5,000 dividend reinvestment participants, also offers direct stock purchase. However, Bank of Hawaii requires prospective shareholders to make their initial purchase through a broker rather than the company. Once a position in the stock is established, investors' subsequent purchases need to be for at least $25 per transaction. Bank of Hawaii spokesman Stafford Kiguchi said the company stopped accepting initial stock purchases last year because it was unpopular and not cost effective. The company's stock currently yields 2.50 percent.

Alexander & Baldwin Inc., with about 650 participants, also offers dividend reinvestment but stipulates that shareholders must own at least 25 shares to be eligible to participate. The company, which requires the initial shares to be purchased through a broker, does not have a direct stock purchase plan. Its stock currently yields 3.86 percent.

In the Hawaiian Electric and A&B reinvestment plans, shareholders are required to be the record holders of the stock as opposed to, for example, a brokerage, which would hold the shares in "street" name. Bank of Hawaii requires shareholders to be either the owner of record or to have a nominee, such as a brokerage, participate in the shareholder's behalf.

"For the smaller investor, the dividend reinvestment plan gives them a chance to buy into the company at a low cost," said Laurie Loo-Ogata, director of shareholder services for Hawaiian Electric. "When you buy from a broker, you generally don't get a break on the commission unless you buy a large number of shares. The (DRIP) is an easy way to slowly accumulate more shares in the company. Also, our dividend yield is really good now compared to other interest rates that are out there."

Hawaiian Electric, which began its reinvestment plan in 1978, has paid dividends continuously since 1901. Currently, it pays 62 cents a share per quarter, meaning that a person with 100 shares of stock would earn $248 a year. The dividend, which has stayed at 62 cents for the last 19 quarters, currently yields 5.43 percent.

Other companies that offer dividends have refrained from initiating dividend reinvestment or direct stock purchase plans because of the administrative costs, lack of demand, or both.

"It's more of a benefit to the stockholder," Loo-Ogata said. "It tends to be a little costly to maintain than just mailing out dividend checks."

In Hawaiian Electric's case, plan participants who reinvest their dividends are charged a service fee of 50 cents per calendar quarter.

There is no brokerage commission to reinvest dividends or buy additional shares if Hawaiian Electric issues new shares, which it is currently doing. However, there is a brokerage commission of 3 cents a share if Hawaiian Electric buys them on the open market. The shares are purchased twice a month. To sell the shares through Hawaiian Electric, there is a $15 service fee plus a brokerage commission of 3.2 cents a share.

Meanwhile, four other Hawaii companies -- ML Macadamia Orchards LP, Central Pacific Bank parent CPB Inc., City Bank parent CB Bancshares Inc. and Barnwell Industries Inc. -- offer dividends but no reinvestment or direct stock purchase plans.

ML Macadamia, which is a partnership rather than a corporation, currently offers a 5.87 percent annual payout to shareholders that is nontaxable because it falls under different Internal Revenue Service regulations. Additionally, the partnership itself is not subject to federal and state income taxes.

"The shares are referred to as partnership units and the dividend, which is called a distribution, is considered a return of capital," said Dennis Simonis, president and chief operating officer of ML Macadamia Orchards. "Essentially, you're getting some of your ownership back. What is taxable to the unitholder is his or her share in the taxable income of the company. The basis goes up when we make money and goes down when we distribute money."

At the current dividend payout of 20 cents a share for the year, or $20 for every 100 shares, unitholders are taxed on only 60 to 65 cents on the dollar because the company's taxable income is lower on a per-share basis than the distribution it pays per share.

As for the other dividend-paying companies, CPB offers a 2.04 percent yield and CB Bancshares a 1.01 percent yield. Barnwell, whose yield is .75 percent, pays its dividends on an irregular basis and has paid just one so far this year after distributing three in 2001.

Morgan Stanley's Loo, who has been in the market for more than 50 years, said one reason why investors shifted to growth stocks during the bull market was for the tax advantage. The capital gains tax for stocks held more than a year is now 20 percent for federal and 7.25 percent for state. Dividends, on the other hand, get taxed as ordinary income. In 2001, those rates were as high as 39.1 percent for federal and 8.5 percent for state.

Consequently, investors' interest in growth stocks has changed the way many companies now distribute some of their earnings. Instead of increasing dividends, many companies use that earmarked money for expansion and to buy back shares on the open market in order to increase the stock price.

"Buying back shares does two things," Loo said. "It supports the stock and reduces the number of shares outstanding so the next dollar of earnings isn't split so many ways. That's a fancy way for the per-share earnings to go up by reducing the available shares."

Ultimately, the higher stock prices benefit long-term investors who can take advantage of the lower capital gains tax rates. Still, Loo said, Congress needs to take a look at helping dividend-conscious investors as well.

"I wish that Congress would make it more attractive for us to enjoy dividends for which we are penalized rather than force us all into capital gains with a favorable tax rate," Loo said. "I read in The Economist (magazine) that more than half of the dividends from stocks on the New York Stock Exchange go to people over 50 years old. That's not unusual because someone who's 55 years old probably would have more stocks than someone who's 22.

"I think Congress should let the older people take the money they've worked so hard for and saved and quit whacking them 40 percent when they finally get their dividends. I think they need to make the dividends less burdensome."

BACK TO TOP

|

NEW YORK >> It sounds like a simple solution for jittery investors: Buy dividend-paying stocks and you'll be assured a payout in return. Dividends still

carry risksPayouts are promises,

not guaranteed moneyAssociated Press

Not all dividends, though, yield easy money.

There are plenty of risks in stocks that pay dividends, and investors who don't understand that might be in for a big surprise when they don't get the returns they expected.

"What many people fail to realize is that dividends are just promises, not guarantees," said Arnie Kaufman, editor of the Standard & Poor's newsletter "The Outlook."

A stock dividend is a portion of a company's earnings paid in cash to shareholders, generally every quarter. The dividend yield is the amount of money per share paid to investors divided by the stock price.

For instance, if you owned 100 shares of a company's stock and received 25 cents each quarter for each share, then the total dividend payment would be $100 for the year. With a stock price of $50, annual dividend yield would be 2 percent.

Conservative, stable companies like McDonald's and Philip Morris have long paid dividends, giving back to shareholders at least some of their profits and then reinvesting the rest in their businesses.

Dividends became passe in the 1990s tech boom, when investors chased after young companies with soaring stock prices that shunned dividends in favor of plunging money back into their operations.

Now, thanks to Wall Street's two-year tumble, investors are clamoring for dividends again. But buying a stock just because it pays a dividend is a dangerous tactic. The key is to figure out whether the payout will last.

The first red flag to look out for: high dividend yields, namely those topping 10 percent to 15 percent.

"Beware when you see a high-paying dividend yield because the reason the company is paying so much is because there is underlying risk," said Mike Thompson, market strategist for the financial analytics firm RiskMetrics Group.

When it comes to a stock with a high yield, Thompson suggests looking at the position of the company now and considering what could happen in the future.

Another important factor to consider before buying a dividend-paying stock: how long the company has paid a dividend and how much the payments have changed.