|

Closing Market Report

Star-Bulletin news services

|

Trusting analysts can be dangerous

Conflicts are still a problem, and so are flat-out inaccuracies

By Ellen Simon

Associated Press

NEW YORK » Mocking and maligning analysts has been a sport for investors ever since the Internet bubble burst.

Still, despite public humiliation for a handful of analysts and a $1.44 billion settlement in 2002 involving 10 Wall Street firms' research operations, investors still read analysts' reports, and they still believe them. Whatever conflicts may be behind them, whatever errors may be contained in their pages, analysts' recommendations still move stocks.

The fourth-quarter earnings season was a great lesson in how often analysts' predictions are wrong. Of the Standard & Poor's 500 companies, 204 reported earnings that were higher than expected by 5 percent or more, while 60 companies reported earnings that were below expectations by 5 percent or more, according to Zacks Investment Research Inc. That means analysts estimates were off by 5 percent or greater more than half the time last quarter.

The fourth-quarter earnings season was a great lesson in how often analysts' predictions are wrong. Of the Standard & Poor's 500 companies, 204 reported earnings that were higher than expected by 5 percent or more, while 60 companies reported earnings that were below expectations by 5 percent or more, according to Zacks Investment Research Inc. That means analysts estimates were off by 5 percent or greater more than half the time last quarter.

The reports have other flaws investors should keep in mind:

» Analysts are still overwhelmingly positive.

Zacks ran the numbers on the average broker rating of the 4,527 companies it follows; 42 percent of the companies had an average rating of "Buy" or "Strong Buy." Only 3 percent had ratings of "Sell" or "Strong Sell." Considering that many of those "Sell" ratings are on companies that are already in big -- and public -- trouble, the ratings look even less useful.

» Consider the source.

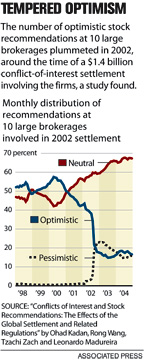

The 10 large investment banks that negotiated a 2002 $1.44 billion settlement with the New York Attorney General, the Securities and Exchange Commission and other regulators over their biased stock ratings may have changed their behavior, to a degree.

A paper called "Conflicts of Interest and Stock Recommendations: The Effects of the Global Settlement and Related Regulations" found that analysts at the 10 firms that were part of the settlement were more likely to issue pessimistic recommendations than other analysts.

But the real surge at the 10 firms covered by the agreement has been in "Hold" rankings on stocks, which have soared, while "Buy" rankings have dropped.

If there's a relationship between the bank and the company it covers, beware. Tzachi Zach, an assistant professor of accounting at the John M. Olin School of Business at Washington University in St. Louis and one of the paper's four authors, said, "We still observe some reluctance on the part of analysts who are somehow related to a firm (they cover) to issue pessimistic forecasts, sell recommendations."

Finally, a recent article in the "Journal of Accounting and Economics" found that forecasts by full-service banks are less optimistic than those by analysts at other firms. The most optimistic forecasts came from brokerage firms.

» Look for revisions.

The overwhelmingly positive nature of analyst ratings makes a downward revision in a company's rating more notable.

"If you've got a group of people who are largely bullish on pretty much everything and they start getting less bullish, that's something I want to take note of," said Kevin Matras, manager of the Research Wizard division at Zacks.

» Remember that companies that beat analysts' estimates one quarter are likely to beat again another quarter.

Forget the noise on the day a company announces earnings, but look to see if a company could be establishing a pattern.

"It may be a situation where you thought it was a good company and it turned out great, or it could be a situation where you thought it was awful and it turned our mediocre," Dirk Van Dijk, research director at Zacks. "You can make a lot of money off the stocks everyone thought were awful that turned out to be just mediocre."

» Look for a change in the number of analysts covering a stock.

More coverage is a bullish sign and less coverage is a bearish sign. Looking for added coverage may be a way to find smaller stocks that are on the move, Matras said.

"If a stock has one analyst covering it or no analysts and it suddenly has a couple analysts covering it, it makes you think something may be going on here," he said.

» Finally, don't assume analysts are using the correct financial data about the companies they cover.

Christopher Cox, chairman of the Securities and Exchange Commission, said in a March 3 speech: "Executives who have taken the time to double-check the data that financial analysts following their companies are working with can sometimes get quite a shock. That's because some of them bear no resemblance to what the companies published."

According to Cox, manual rekeying of information from financial statements produces an error rate that is unacceptably high. Numbers analysts use in valuation models can have an error rate of 28 percent, he said. The rate can be even higher if the data in question comes from the footnotes.

So, how valuable are analysts' reports?

Mark A. Chen, an assistant professor of finance at the Robert H. Smith School of Business at the University of Maryland, has studied analysts' conflicts.

While Chen found almost no evidence of bias or conflicts when it came to short-term quarterly earnings forecasts and the accuracy of reports, he said "If I were to invest, I would probably not rely on analysts' recommendations; or, if I did, I would take them with a grain of salt. Which is not to say there is no information there; it just has to be taken with caution."